Private Credit's Ascent: A Reshaping of Modern Lending Markets

Institutional Appetite, Yield Engineering, and the Rise of Shadow Banking 2.0

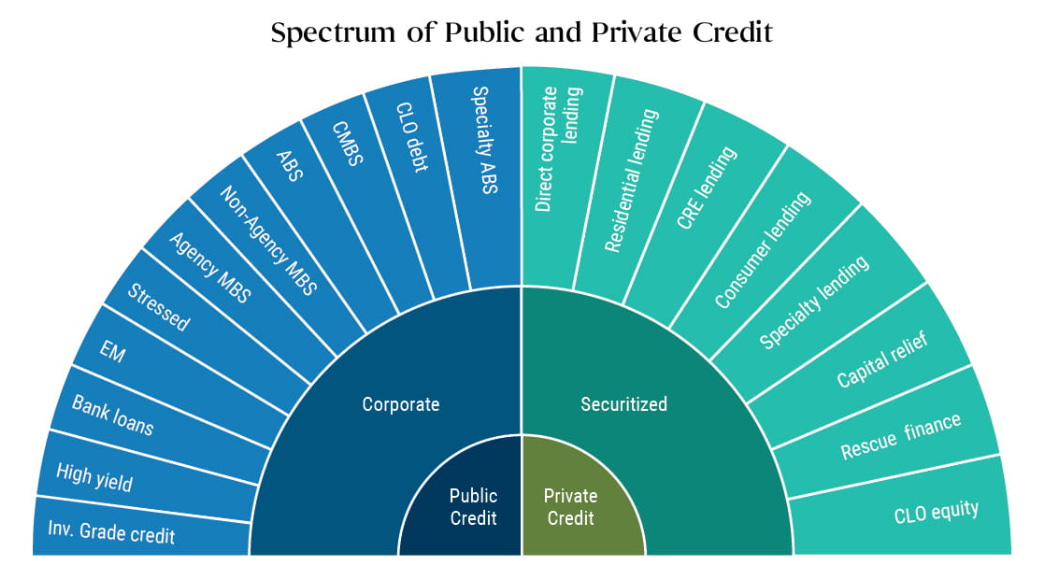

Executive Brief

Private credit—once a niche corner of the fixed income universe—has surged into the mainstream, now commanding over $1.7 trillion in assets globally, with projections surpassing $2.3 trillion by 2027. As traditional bank lending retrenches under regulatory pressure, institutional investors—ranging from pensions to sovereign wealth funds—are pivoting heavily into this opaque but lucrative sector.

This SignalVest Insight dissects the structural catalysts, risk undercurrents, and tactical implications surrounding the meteoric rise of private credit. We also analyze the strategic positioning of key players, explore regulatory developments, and identify asymmetric trade opportunities across public proxies and deal flow ecosystems.

Why Now? Structural Shifts Driving the Surge

Banking Retreat → Direct Lending Boom

Basel III and post-GFC regulations have curtailed banks’ balance sheet flexibility, particularly for leveraged loans and sub-investment grade borrowers. Private credit funds have moved in aggressively, offering customized, covenant-light lending solutions.Yield-Starved Institutions

Despite rising interest rates, traditional fixed income still struggles to deliver long-duration yield aligned with actuarial targets. Private credit, by contrast, offers 8–12% unlevered yields—often with floating-rate mechanics and collateralization.Liquidity Premium Mispricing

Investors are betting that the illiquidity premium embedded in private deals remains underappreciated relative to default-adjusted risk. This is especially true in middle-market lending, where competition from banks has virtually evaporated.

Tactical Allocations: How to Play the Theme

Public BDCs (Business Development Companies)

Liquid proxies like ARCC, GBDC, and FSK provide transparent access to diversified private credit portfolios.

Watch for NAV discount arbitrage, dividend coverage, and leverage sensitivity.

Structured Credit ETFs

Products such as JAAA (Janus Henderson AAA CLO ETF) or OXLC offer yield exposure with varying credit tranching.

Secondaries & Distressed Entry Points

In downturns, expect forced sellers in the secondary private loan market. This creates an asymmetric opportunity for distressed allocators.

Private Funds / SMA Mandates

Family offices and institutional LPs can pursue direct exposure via co-investments, club deals, or SMAs with top-tier credit managers.

SignalVest Final Take

Private credit is no longer an "alternative"—it is a core pillar of modern institutional portfolios. While the asset class offers compelling yield and diversification benefits, the risks embedded in liquidity mismatches, underwriting opacity, and leverage mechanics warrant active surveillance.

At SignalVest, we believe a bifurcated approach is optimal: tactical exposure via liquid proxies for flexibility, and selective allocations into well-governed private vehicles for core yield.

As the market matures, expect consolidation among platforms, greater regulatory oversight, and an eventual correction in overly aggressive vintages. Timing and underwriting discipline will be critical to avoiding the next vintage trap.