SignalVest Daily // Issue #001

When The Filings Don’t Match the Headlines: A Forensic Look at BigBear.ai (NYSE: BBAI)

“There are no bad assets, only bad prices.” - GMO

BigBear.ai (NYSE: BBAI) is one of those companies that the market either forgets or gets obsessed with—rarely anything in between. In early 2023, the stock surged on AI hype, defense contracts, and speculation surrounding its ties to Palantir-like themes. But the run didn’t last, and now it’s quietly re-emerging in a way that forces us to take another look—not as bulls or bears, but as forensic analysts trying to decode capital structure intentions.

Let’s be clear: this is not about product-market fit. It’s about what management does when no one’s looking.

What’s Happening Under the Surface?

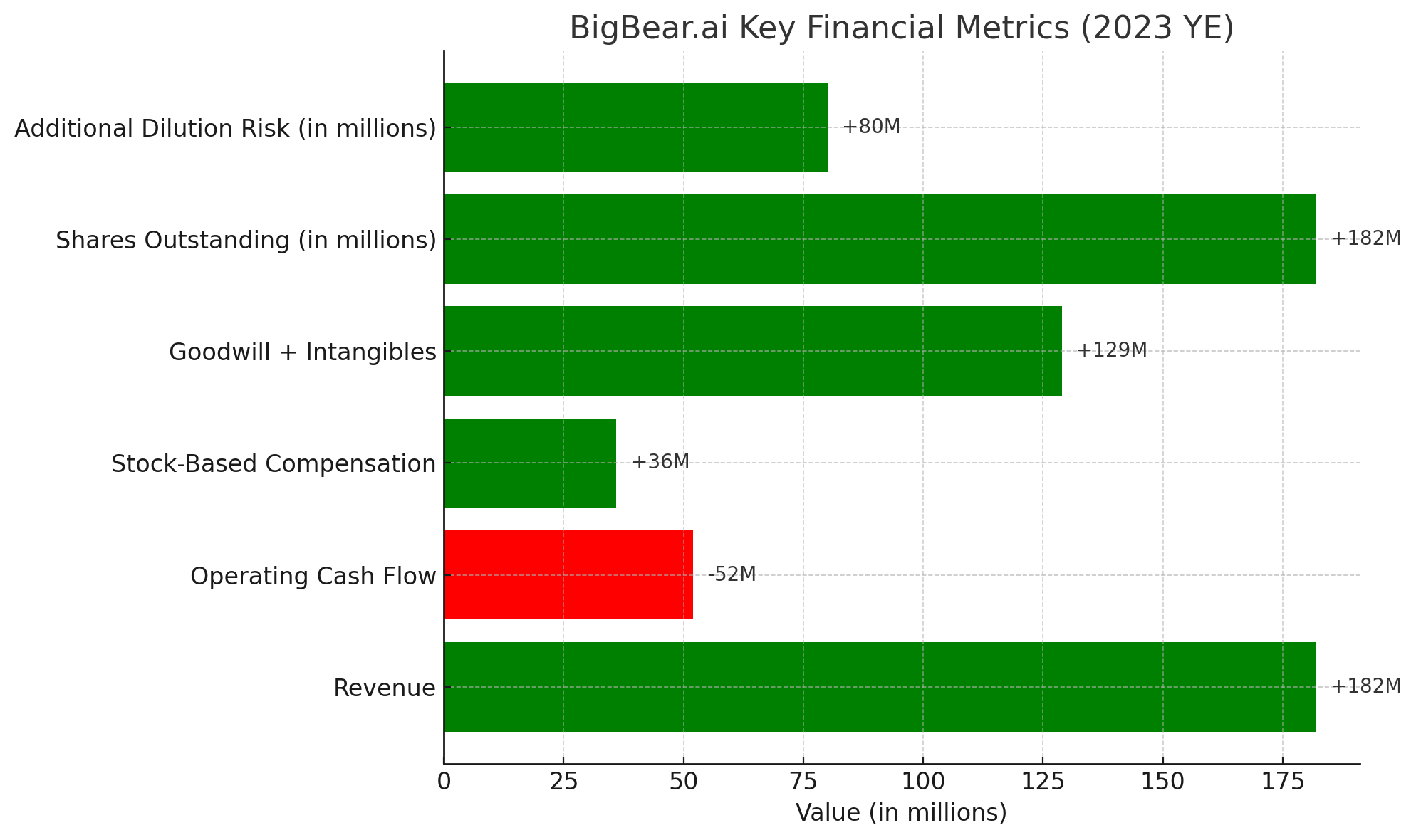

In March 2024, BigBear.ai announced a new $25 million equity offering, following a previous $200M ATM program that quietly diluted long-term holders by more than 60%. On the surface, the justification was to “invest in growth” — a term so loosely applied it should raise regulatory eyebrows.

But the filings tell a different story.

In the latest 10-K, BigBear.ai admitted it has recurring negative operating cash flow, and cash on hand dipped below $35 million — despite grossing over $180 million in revenue.

Stock-based compensation was $36 million in 2023, almost matching gross profit.

The ATM from 2023 was largely exercised at prices between $1.25 and $2.00. Today, the stock trades closer to $1.15 — and now they’re back for more.

It doesn’t end there.

SignalVest Forensic Take

This setup follows a pattern we’ve flagged repeatedly at SignalVest:

Equity-led lifelines while the core business stalls

Promotional narratives (AI, defense, geopolitics) recycled near offering windows

Insider enrichment through options issuance at suppressed prices

Retail apathy creates illiquidity, which forces additional discounts on new rounds

BigBear.ai’s balance sheet today is a Frankenstein of warrant liabilities, goodwill bloat, and adjusted EBITDA acrobatics. It doesn’t resemble a scalable AI defense firm — it resembles a reverse-engineered SPAC play looking to survive long enough to get bought.

If the company were serious about long-term compounding, SBC would trend down, not up.

If the product-market traction was real, revenue would scale faster than dilution.

What the Market Misses

Everyone’s watching the macro: rates, defense spending, AI narrative flows. But few are watching the next 6 months of funding mechanics, which is where risk hides.

Here’s the asymmetry:

The market is pricing BBAI like an AI-driven turnaround, but their capital behavior suggests a financing-driven survival plan.

If the new equity raise is exercised in full and existing warrants are executed at discounted levels, the float could increase by another 80–100 million shares in 2024.

This dilution, paired with insider options repriced at lower levels, could anchor the stock sub-$1, even in a risk-on rally.

Summary Table

SignalVest Red Flag Intelligence Score: 7.8 / 10 – “Elevated Risk”

Final Thought

There’s a market for stories and a market for substance. BigBear.ai is currently trading somewhere in between — with just enough narrative to stay alive and just enough dilution to cap upside.

This isn’t a bet on product. It’s a bet on whether retail fatigue outpaces insider urgency.

If you’re holding, trading, or considering the name, be clear on what game you’re playing. The business model may evolve, but the current capital behavior tells us the real play is time and tolerance, not transformation.

—

Want the full Red Flag Screener updated weekly?

Subscribe for access to forensic bulletins, signal-driven alerts, and deep dives on high-risk capital structures.