SignalVest Forensic Risk Report:

Hims & Hers Health (HIMS) – Q1 2025 Update

Hims & Hers Health, Inc. (NYSE: HIMS) is a telehealth and wellness platform that delivered explosive growth through 2024, achieving its first full-year GAAP profitability. However, a forensic analysis flags several red-flag risks despite the strong headline performance.

Financial Highlights (Q1 2025 & FY 2024)

Surging Revenue & Subscriber Growth: FY2024 revenue reached $1.5 billion (up 69% YoY), driven by expanding telehealth offerings (e.g. primary care, dermatology, and newly weight management). Subscribers grew to 2.2 million (+45% YoY), reflecting successful customer acquisition efforts. Q4 2024 saw strong momentum, prompting FY2025 guidance of $2.3–2.4 billion revenue (another ~60% YoY gain).

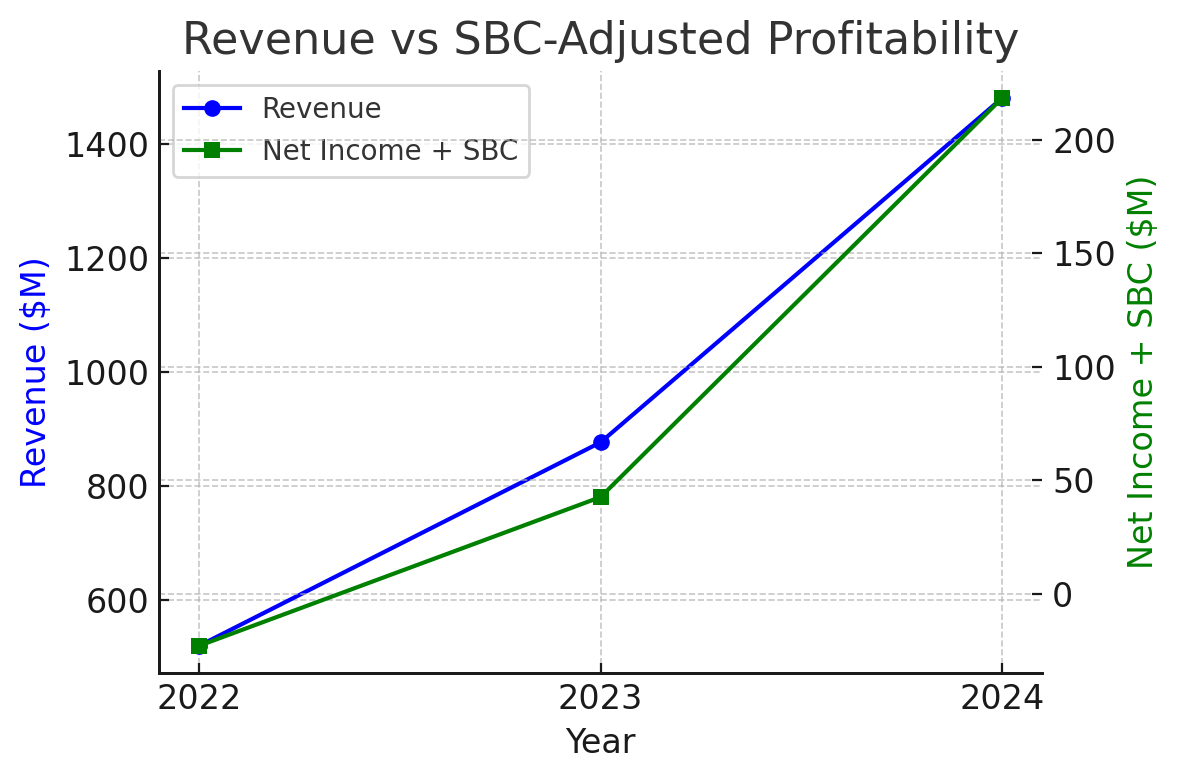

First GAAP Profitability (with Caveats): HIMS reported $126 million net income for 2024 (vs. a $23.5 million loss in 2023) – a sharp turnaround aided by a one-time $61.6 million deferred tax benefit recognized as the company released its valuation allowances. Excluding this tax credit, pre-tax income was more modest (~$64 million). Adjusted EBITDA came in at $177 million, but this excludes significant non-cash costs like SBC. Stock-based compensation expense was $92.3 million in 2024 (up from $66.1 M in 2023), amounting to ~6% of revenue. If we treat SBC as a real cost (as GAAP does), underlying net profit would be substantially lower (or even negative without the tax benefit). The chart below shows revenue growth versus “SBC-adjusted” net income (adding back SBC to net income for comparability):

Chart: Revenue vs. SBC-Adjusted Profitability (2022–2024). Revenue surged ~69% in 2024 to ~$1.5 B, while GAAP net income (green line, with SBC added back) climbed to ~$218 M (including a $61.6 M tax benefit) after prior-year losses. This illustrates improving operating leverage, although ~42% of 2024 profit was from a one-time tax gain and excluding $92 M of stock-based comp expense.

Cash Flow Strength: Despite high SBC and marketing spend, operating cash flow hit $251 million in 2024, buoyed by the net income swing and favorable working capital dynamics (e.g. upfront customer payments). Free cash flow was positive (~$183 M after ~$68 M of capex and an acquisition). The company ended 2024 with $300+ million in liquidity ($220.6 M cash + $79.7 M short-term investments) and no near-term need to raise capital. This cash pile enabled strategic acquisitions and share repurchases without external financing.

Marketing & Margin Trade-off: HIMS aggressively reinvests in growth – marketing expense was $679 million in 2024 (+52% YoY), consuming ~46% of revenue. Customer acquisition costs (the bulk of marketing spend) rose to $594.5 M, indicating HIMS paid heavily to add subscribers. Gross margins remain high (benefiting from a digital model and vertical integration), but operating margin is thin once marketing and SBC are accounted for. This raises a sustainability question: growth is strong, but reliant on continued heavy marketing spend, albeit with improving ROI (revenue grew faster than marketing cost in 2024). Investors should monitor if HIMS can scale back marketing intensity and maintain growth or if a growth slowdown might reveal the true earnings power.

Share Count & Dilution Analysis

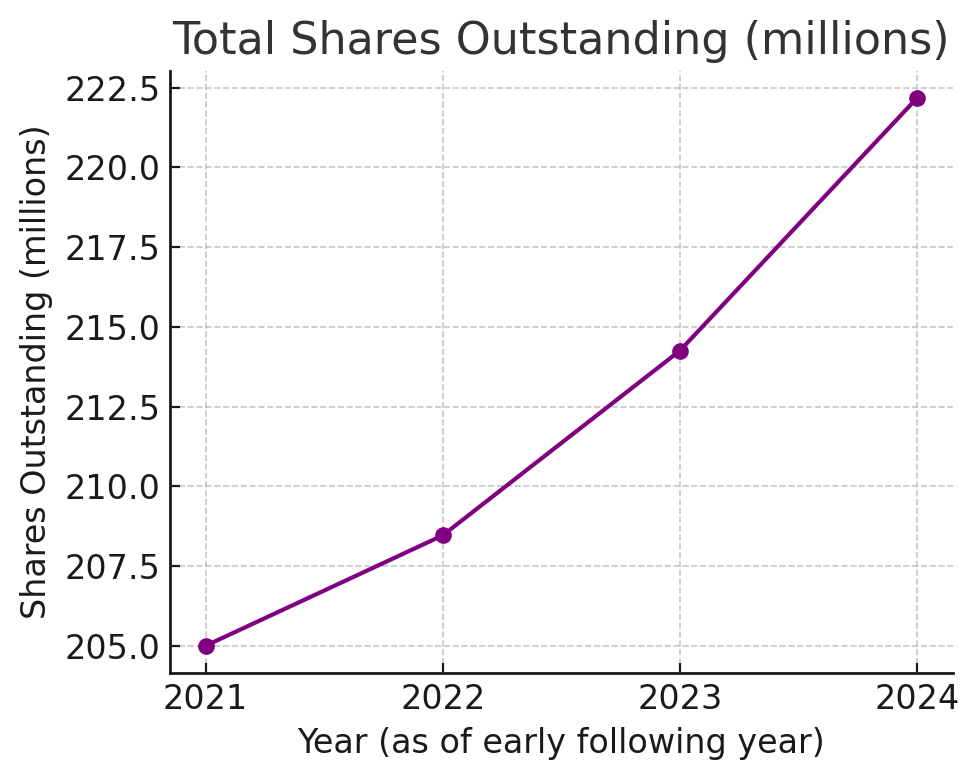

Dilution Mapping: Since its January 2021 SPAC merger, Hims & Hers’ share count has steadily increased – despite a stock buyback program – due to employee equity grants, warrant exercises, and earn-outs. Total shares outstanding rose from ~208 million (Feb 2023) to ~222 million (Feb 2025) (including Class A and Class V shares), a ~7% increase over two years. The timeline below highlights the trend:

Chart: Total Shares Outstanding (millions). HIMS’s share count expanded from ~205 M in 2021 (post-SPAC) to ~222 M by early 2025 despite share repurchases. Outstanding Class A shares grew by ~8 M from Feb 2023 to Feb 2025, reflecting net dilution from stock-based compensation and other issuances, partially offset by buybacks.

Stock-Based Compensation: SBC is a major dilution driver. In 2024, employees were granted or exercised rights to millions of shares. Example: 4.4 million shares were issued upon RSU vesting in 2024 (net of tax withholdings) on top of stock option exercises (~$2.3 M cash received). The employee stock purchase plan (ESPP) added ~0.62 M shares in 2024. While SBC helps conserve cash, it dilutes equity – though HIMS’s soaring stock price has made these grants very valuable to insiders (see below).

Share Repurchases: In contrast to many high-growth tech firms, HIMS instituted buybacks to counter dilution. The board authorized $50 M in late 2023 and an additional $100 M in 2024 for repurchases. By Dec 31, 2024, the company had repurchased ~3.63 M shares under the 2023 program and ~$35 M (approx 1.7–2.0 M shares at prevailing prices) under the 2024 program. In total, $83 M was spent in 2024 on buybacks. These repurchases partially offset new issuance – a shareholder-friendly move – but not entirely: net share count still climbed as noted. Notably, HIMS repurchased shares in mid-2024 when prices were much lower (e.g. ~$10–20 range), which rewarded the company now that shares trade higher.

Options, Warrants & Earn-outs: As of year-end 2024, ~0.27 M legacy vendor warrants remained outstanding (avg. exercise price $1.75) – these are in-the-money and likely to convert to stock (a batch of 190k was exercised in Dec 2024). Upon exercise, vendors also receive earn-out shares (e.g. 18.6k extra shares were issued in Dec for one holder). These warrants are a small overhang. Additionally, an earlier set of debt-related warrants (exercise $6.96) were net exercised in 2024, yielding ~52.6k shares plus 9.7k earn-out shares. On the employee side, HIMS’ equity incentive plans still have many unvested RSUs and stock options that will vest in coming years, contributing to future dilution (though the company may continue using buybacks to offset). Investors should expect share count to keep drifting upward but at a manageable pace; the dilution “heatmap” appears moderate compared to many tech peers, thanks to the offsetting buybacks and relatively limited warrant overhang.

Capital Raises: Importantly, HIMS has not needed to raise equity capital recently. It filed a mixed shelf registration (Form S-3ASR) in late 2024, giving flexibility to issue securities (common stock, etc.) over time – but this is a routine move for a well-capitalized seasoned issuer (market cap ~$6 B by early 2025). There have been no secondary stock offerings or new dilutive financings in 2024–Q1’25; in fact, HIMS funded a small acquisition (MedisourceRx) and facility purchases from cash on hand. Unless a major M&A arises, further share issuance via the shelf is unlikely near-term given the strong cash flow profile.

Bottom line: Dilution risk exists (as visualized above) but is relatively under control – share count growth (~3–4% per year) is far slower than revenue growth. The dilution “heat” peaked in 2021–2022 as the SPAC merger and early SBC hit, and has since cooled with the aid of buybacks. However, investors should remain vigilant: continued high SBC (>$90 M/year) is effectively a recurring equity cost, and any renewed capital raising or M&A paid in shares could accelerate dilution. The company’s proactive buybacks and lack of new stock issuance in 2024 are positive signs on this front.

Insider Transactions & Ownership Red Flags

One of the most striking developments as HIMS stock price soared in early 2025 has been heavy insider selling. Top executives substantially reduced their holdings during Q1 2025, cashing in on the stock’s sharp rise to all-time highs:

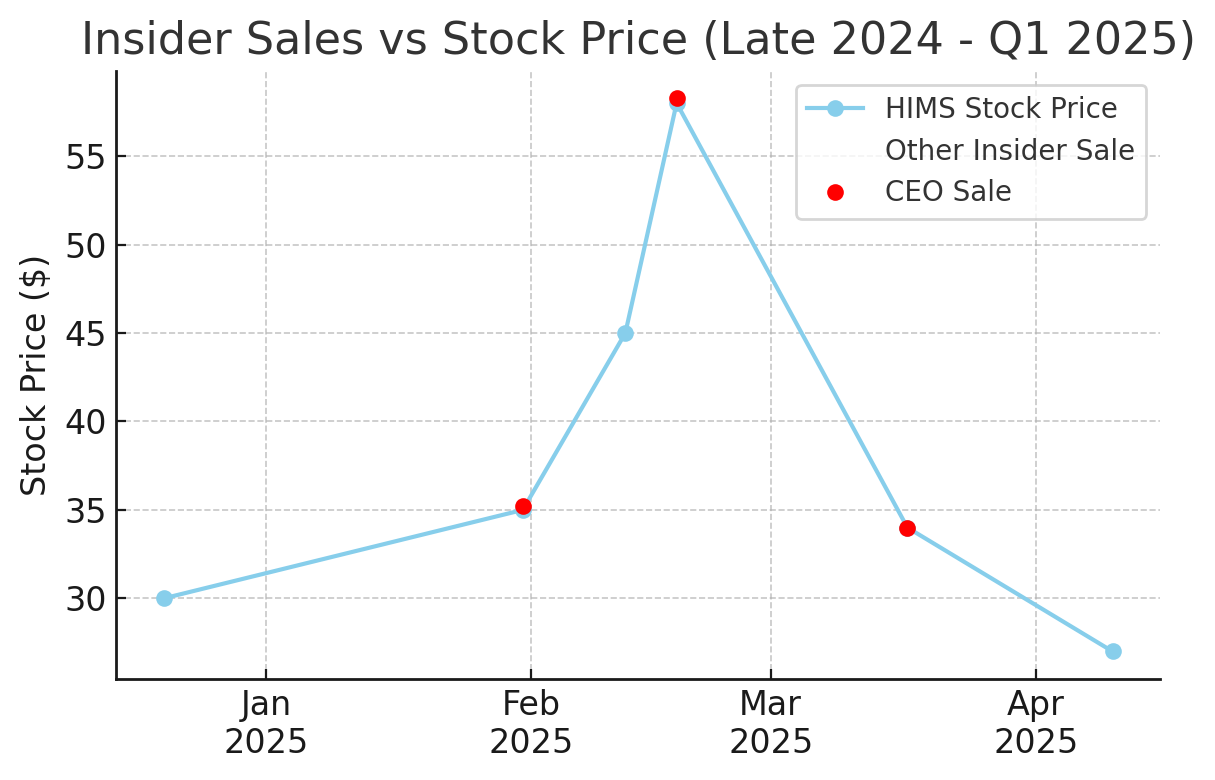

CEO Sales: Co-founder & CEO Andrew Dudum made multiple large stock sales. Notably, on Feb 18, 2025 – with HIMS near its peak of ~$58 – he sold 128,127 shares at $58.27 each, totaling $7.46 million. This was shortly after a sale of 100k shares at ~$35 on Jan 31, 2025, and he sold another 128k shares at ~$34 in mid-March as the stock retreated. These timing of sales (especially the large Feb sale at the peak) could raise eyebrows: insiders often sell on predetermined schedules (10b5-1 plans), but the coincidence with the price top and subsequent decline is notable.

CFO & COO Sales: CFO Oluyemi Okupe and COO Melissa Baird also sold frequently. The CFO sold stock four times in Q1 2025, ranging from ~$38 (Feb 4) to ~$29 (Apr 2), cumulatively tens of thousands of shares. The COO similarly sold ~68k shares at $44.71 on Feb 12, 2025 (for ~$3.0 M), another ~67k at ~$34.84 in late March ( ~$2.36 M), and additional shares in April. Other insiders (General Counsel, directors) were also trimming positions throughout this period.

No Insider Buying: Over the past year, virtually all insider open-market activity has been sales, not purchases. The selling began even in late 2024 – e.g., the CFO sold ~19k shares on Dec 20, 2024 at ~$30 – and intensified as the stock rallied in 2025. This pattern suggests insiders viewed the ~$30–$60 range as an opportune time to take profits or diversify. In the 6 months through early April 2025, insiders executed dozens of sale transactions and zero buys, signaling insider confidence may have plateaued at higher valuations.

Chart: Insider Sales vs. Stock Price (Late 2024 – Q1 2025). As HIMS stock rocketed ~100%+ from late-2024 into early-2025, insiders unloaded shares aggressively. Red dots mark CEO sales (e.g. ~128k shares at ~$58 in Feb 2025), and orange X’s mark CFO/COO. The stock peaked in mid-February, shortly after which insiders continued selling as the price declined. Such clustered selling can be a red flag, though sales may be pre-scheduled.

Insider Ownership & Control: Post-SPAC, Hims & Hers has a dual-class structure – Class V shares (held by founders) carry super-voting rights. Andrew Dudum retains 8,377,623 Class V shares (unchanged from 2021 to 2025), which give him outsized voting power (each Class V had 1 vote vs. Class A’s 1 vote, and collectively Class V represented ~3.7% of total shares but a larger % of votes). This means insiders can sell a portion of their economic stake while still controlling the company via voting rights – a governance risk if insider incentives diverge from shareholders’. So far, Dudum’s Class V stake suggests he remains invested in HIMS’s long-term value (he cannot sell those without converting to Class A), but public investors should be mindful that voting control is concentrated.

Implication: While insider selling doesn’t necessarily signal a top (executives may sell for diversification or tax reasons), the magnitude and timing here warrant caution. SignalVest Forensic Flag: Insiders “selling into strength” at record prices, especially the CEO’s large sale near peak, is typically a bearish indicator. It suggests those closest to the company deemed the valuation rich enough to harvest gains. Coupled with the fact that insiders are not buying on dips, this insider behavior raises a red flag about management’s true confidence in the next leg of HIMS’s growth or stock upside. Shareholders should closely watch subsequent SEC Form 4 filings for any continued selling or, conversely, any insider buying which could restore confidence.

Financial Statement Quality & Forensic Considerations

Beyond the surface-level earnings, a forensic look at HIMS’s financials highlights a few areas of note:

One-Time Items Boosting Income: As mentioned, 2024’s net income was bolstered by a $61.6 M one-time tax benefit (from reversing a deferred tax asset allowance due to anticipated profitability). This non-recurring accounting gain comprised ~49% of pre-tax income, meaning true operating profit was much lower. Without it, HIMS might have only roughly broken even or had a small profit in 2024. Investors should not extrapolate the $126 M net income blindly – future effective tax rates will normalize (guidance implies a small tax expense in 2025). Forensic flag: quality of earnings is somewhat low given reliance on a tax accounting reversal rather than purely operational results.

Stock-Based Comp “Hidden” Cost: While SBC is fully expensed under GAAP, management (and some analysts) often focus on Adjusted EBITDA which excludes SBC. In HIMS’s case, adding back SBC makes EBITDA look much higher ($177 M), but SBC is a real cost to shareholders (dilution). If we subtract SBC from EBITDA to get a true cash profit after compensating employees, 2024’s ~$85 M (177–92) is far below the touted $177 M. The chart above showed that only by 2024 did “net income + SBC” turn strongly positive – prior to that, SBC outstripped profits (e.g. 2022 net loss $65.7 M plus SBC $42.8 M = -$22.9 M) meaning the business was not covering the cost of stock grants. The positive trend is favorable (by 2024 OCF > SBC by 2.7x), but forensic investors will monitor SBC closely: if it continues rising or if performance falters, reported profits could vanish once SBC is factored in. Ideally, HIMS should start reducing SBC as a % of revenue (6.2% in 2024) as it matures.

Revenue Recognition & Deferred Revenue: HIMS sells subscription-like services (for example, monthly treatment plans). The 10-K indicates some customers are billed periodically in advance. In 2024, deferred revenue increased, contributing to positive operating cash flow (cash collected for services not yet delivered). This is normal for a subscription model, but it means part of 2024’s cash flow is for obligations to be fulfilled in 2025. We found no evidence of aggressive revenue recognition cut-offs or channel-stuffing – revenue growth aligns with subscriber growth. However, the quality of revenue bears monitoring as the product mix shifts (e.g. one-time kit sales vs. recurring subscriptions vs. in-person services via affiliates could have different margins and revenue timing).

Expense Capitalization: The financials show $11.1 M capitalized website/software development costs in 2024. This suggests HIMS is deferring some expenses (internally developed software) to amortize later. This is acceptable under GAAP (for development beyond preliminary project stage) but can boost current profits. The amount is modest relative to R&D/tech expenses, but a forensic eye will ensure these capitalized costs are not excessive. HIMS’s adjusted EBITDA adds back the amortization of these costs, which is minor so far.

Audit & Controls: The 2024 10-K did not report any material weakness in internal controls, and Big 4 auditor involvement gives some comfort. No restatements or accounting issues have surfaced. The only noteworthy “estimates” were the tax asset valuation (revised in 2024) and fair value of earn-out liabilities (which didn’t materially swing earnings). Thus, apart from the aforementioned items, financial reporting risk appears low – HIMS’s books seem clean, with losses turning to profits largely due to genuine scale economies (gross profit grew dramatically) rather than accounting tricks.

Overall, Hims & Hers’s financial statements reflect a rapidly scaling business with improving fundamentals, but forensic analysis reminds us that true profitability is still emerging when one strips out temporary boosts and includes all costs. The company’s ability to sustain positive free cash flow and profits in 2025–26 without heavy adjustments will be the real test.

Regulatory & Legal Risk Exposure

Perhaps the most significant risk area for HIMS as of Q1 2025 is the evolving regulatory and legal landscape, especially around its new weight loss business (GLP-1 medications like semaglutide):

GLP-1 Compounding Under Scrutiny: In 2024, Hims & Hers launched a popular weight management offering, initially using compounded semaglutide (GLP-1) due to shortages of branded drugs (Ozempic, Wegovy). They even acquired a 503B compounding pharmacy (MedisourceRx) in Sept 2024 and a peptide compounding facility in Feb 2025 to secure supply. However, this opportunistic move comes with high regulatory risk. By law, compounding of a drug like semaglutide is only allowed while it’s on FDA’s shortage list. The FDA resolved the semaglutide shortage on Feb 21, 2025, which “could constrain [HIMS’s] ability to continue providing access to compounded semaglutide” once current inventory is sold. Simply put, HIMS may soon have to cease selling compounded (cheaper) semaglutide, forcing patients to buy expensive branded versions or HIMS to find alternative solutions. The 10-K explicitly warns that they “cannot guarantee” being able to keep offering these products and that this could adversely affect the business.

FDA & Lawsuit Risks: The compounding industry is lobbying to maintain access – e.g. an industry group filed a lawsuit against the FDA when it removed another GLP-1 (tirzepatide) from the shortage list. That lawsuit is ongoing as of Feb 24, 2025, but the FDA has thus far reaffirmed its stance. Additionally, Novo Nordisk (maker of Ozempic/Wegovy) petitioned FDA to ban compounding of semaglutide outright by putting it on a “Difficult to Compound” list. If FDA agrees, HIMS’s ability to customize these meds would end permanently. Moreover, 503B compounding facilities face intense FDA and state scrutiny due to past quality issues in the industry. Any violation at HIMS’s pharmacies (or their partners) could trigger enforcement actions or lawsuits, impacting HIMS’s reputation and finances. This is a high regulatory compliance risk introduced by the new vertical – essentially HIMS ventured into a partially gray area of pharmacy law to meet demand, and regulators may crack down.

Telehealth Regulation & State Laws: HIMS’s core model of prescribing online has to navigate varying state telemedicine laws, physician licensing, and possible future federal rules. The COVID-era flexibility boosted telehealth, but there’s always a risk of regulatory rollback. The company notes it relies on affiliated medical groups and independent contractor doctors in all 50 states. If states impose tighter telehealth rules or require physicians to have in-person exams for certain prescriptions, HIMS’s model could be disrupted. For example, the DEA has been evaluating whether to end the pandemic policy that allowed controlled substances to be prescribed via telehealth without an initial in-person visit. Any such changes could require HIMS to adjust operations (though most of HIMS’s products are not Schedule II controlled substances, some weight-loss drugs might be). HIMS must also ensure compliance with online pharmacy laws and the Ryan Haight Act (which governs internet prescription of controlled substances). So far, HIMS appears compliant and proactive in lobbying, but regulatory uncertainty remains a constant risk.

Privacy & Data Security: Handling medical data means HIPAA compliance is mandatory. A breach of patient data or violation of privacy laws (now expanding at state levels) could lead to penalties and loss of consumer trust. There have been no reported major data breaches at HIMS, but it’s a general risk to note. Similarly, any issues with prescription quality or adverse events could lead to malpractice suits or product liability (especially as HIMS expands into treatments like acne meds, hair loss meds, etc., which can have side effects).

Litigation and Settlements: HIMS faced a few legal matters: the 10-K mentions a $2.0 M legal settlement expense in 2024, though details aren’t specified (possibly a minor class action or contract dispute). No material ongoing litigation against the company is disclosed, aside from the industry lawsuit vs FDA (which is not directly against HIMS but relevant). Intellectual property litigation risk is low (HIMS sells mostly generic meds and its branding is unique enough). Regulatory investigations are a bigger concern – e.g., if an attorney general looked into HIMS’s marketing claims or if the FTC examined subscription practices. So far, nothing public on these fronts, but the risk radar for legal issues has certainly increased with the new pharmacy acquisitions.

In summary, Regulatory/Legal risk is arguably the top red flag for HIMS in 2025. The company’s expansion into compounded medications, at-home lab testing (via Trybe Labs acquisition in early 2025), and broad telehealth services exposes it to healthcare-specific regulations that are complex and changing. Any adverse regulatory action (FDA, state boards) could significantly impact segments of HIMS’s business. Investors should watch for updates on FDA’s stance on compounding and any need for HIMS to pivot (e.g., partnering with insurance to offer brand-name drugs if compounding is off the table). On the positive side, HIMS’s diversified categories (mental health, primary care, etc.) mean not all revenue is at risk – but weight management has been a key growth driver recently, so this risk is non-trivial.

Red Flag Risk Radar & Conclusion

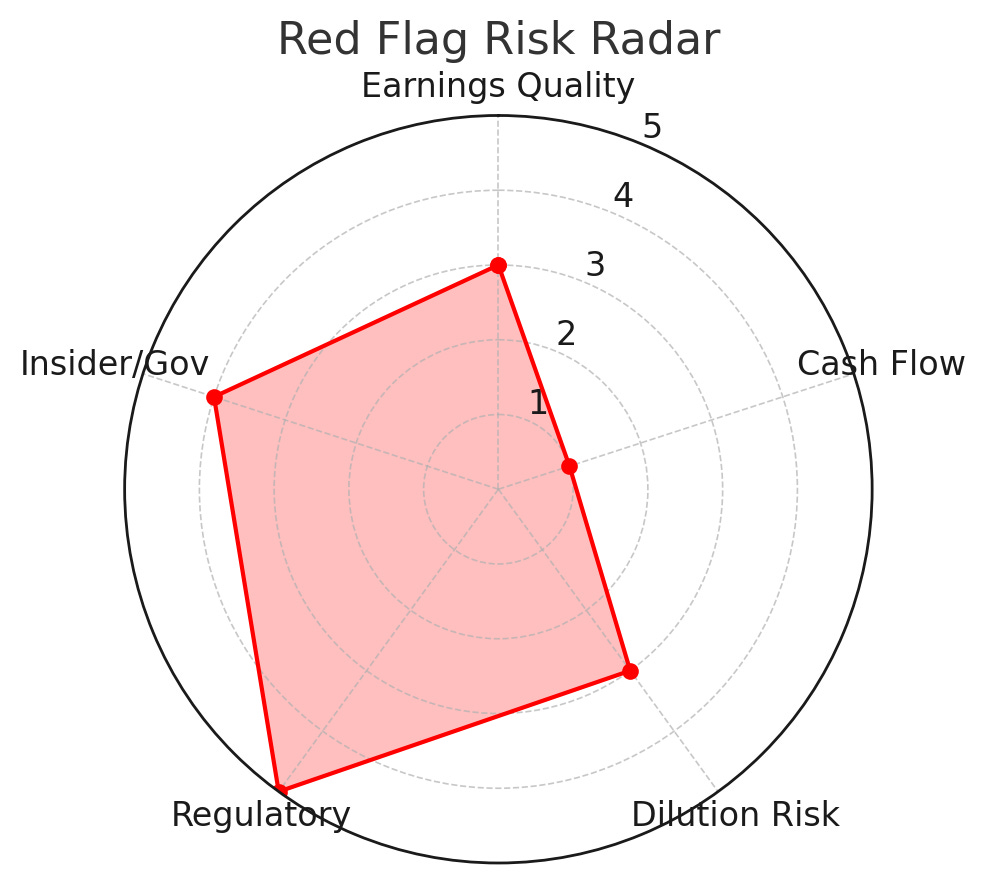

Taking all the above into account, we compile a “Red Flag Radar” – rating key forensic risk categories for Hims & Hers as of Q1 2025:

Visual: Red Flag Risk Radar – Forensic Risk Assessment. Interpretation: Regulatory risk is highest (5/5) given looming FDA constraints on compounding and telehealth rule uncertainties. Insider/Governance risk is elevated (4/5) due to significant insider selling and dual-class control structure. Dilution risk is moderate (3/5); dilution exists but is partly mitigated by buybacks and strong cash flow (hence not as high as many growth peers). Earnings Quality is moderate (3/5) – current profits are real but aided by one-offs and heavy adjustments (we’d like to see sustained GAAP earnings without relying on add-backs). Cash Flow risk is low (1/5) – HIMS’s cash generation and balance sheet are strong, reducing financial distress concerns.*

In conclusion, Hims & Hers Health enters 2025 as a high-growth, now-profitable disruptor with a solid cash foundation, but one that is not without risks. The forensic signals to heed include:

Insiders taking money off the table aggressively into the stock’s strength.

Profitability not fully organic, but aided by accounting benefits and exclusion of hefty SBC costs.

Share dilution continuing (albeit at a reasonable pace), with shareholders relying on management to keep buybacks active to offset employee awards.

Regulatory clouds on the horizon, particularly around one of HIMS’s fastest-growing product lines (compounded GLP-1s) – a risk that could slow momentum or require strategic changes in 2025.

Operational dependence on marketing – can HIMS maintain 60–70% growth and improve margins, or will scaling beyond the “low-hanging fruit” of early adopters raise customer acquisition costs further?

From a SignalVest forensic perspective, these factors warrant a cautious optimism stance. HIMS’s financial “signals” are mixed: on one hand, exceptional growth, improving unit economics, and prudent capital management; on the other, insiders selling and regulatory uncertainties flashing warning signs. Investors should expect heightened volatility – e.g., any news on FDA rulings or insider trade disclosures could swing the stock.

Recommendation for risk-focused investors: closely monitor HIMS’s Q1 2025 10-Q and earnings call (scheduled in coming weeks) for updates on the compounding issue, any changes in subscriber growth vs. marketing spend, and whether management addresses their stock sales or plans for further buybacks. Hims & Hers has navigated start-up losses to reach profitability, but the next test is sustaining that profitability amid external challenges. By keeping a close eye on the red-flag indicators highlighted here – dilution, insider activity, and regulatory developments – investors can better gauge if HIMS’s current lofty valuation is justified or if these forensic risks will eventually weigh on the company’s trajectory.

Sources: Official SEC filings (10-K, 10-Q), HIMS Q4’24 earnings release and shareholder letter, Insider trade filings (Form 4 summarized), and HIMS press releases. All data is current as of April 13, 2025.