SignalVest Insight | Market Breakdown: Macro Dislocations & Institutional Chess Moves

Analyzing Rotational Flows, Tactical Dislocations, and Multi-Asset Repricing Across the Global Investment Landscape

The market narrative entering mid-Q2 2025 is increasingly divergent beneath the surface of headline indices. While the S&P 500 hovers near all-time highs, cracks are emerging across global equity breadth, sovereign bond volatility, and cyclical undercurrents. This week’s report dissects institutional flows, macro dislocations, and silent signals that suggest potential regime change in positioning.

Macro & Market Pulse: Contradictions in the Crosscurrents

Inflation Surprise & Yield Curve Behavior

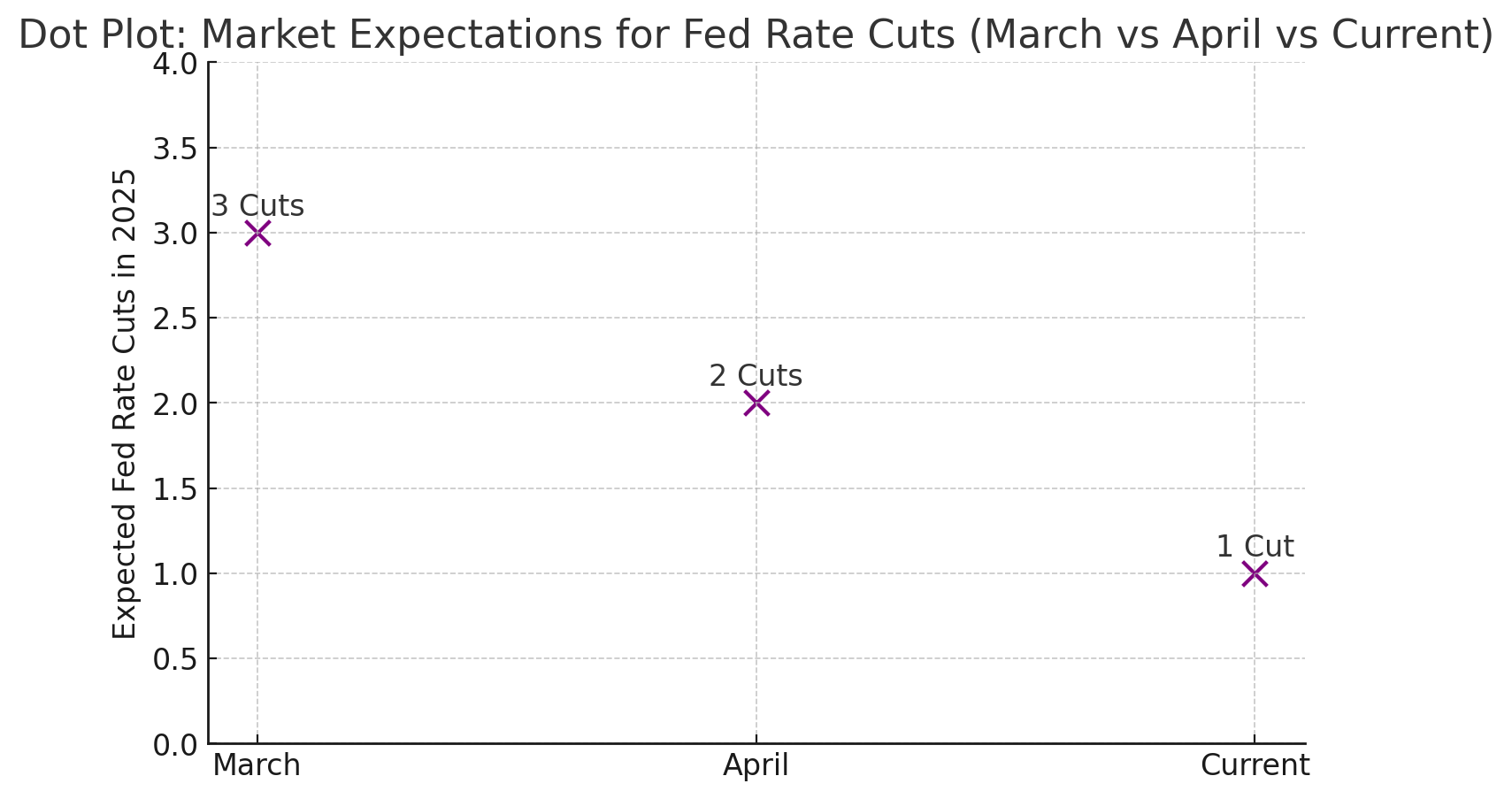

U.S. CPI (March): Core inflation came in hotter than expected at 3.9% YoY, sparking a swift repricing in Fed cut expectations.

Rate Market Reaction: Futures now price only one rate cut in 2025, down from three just 30 days ago.

2s/10s Spread: Still inverted at -35bps, but flattening rapidly as short-end reprices hawkishly.

SignalVest Take: This signals a market struggling to reconcile persistent services inflation with sluggish manufacturing and earnings guidance. A bifurcated economy, where rate sensitivity is sector-specific, creates tactical alpha opportunities.

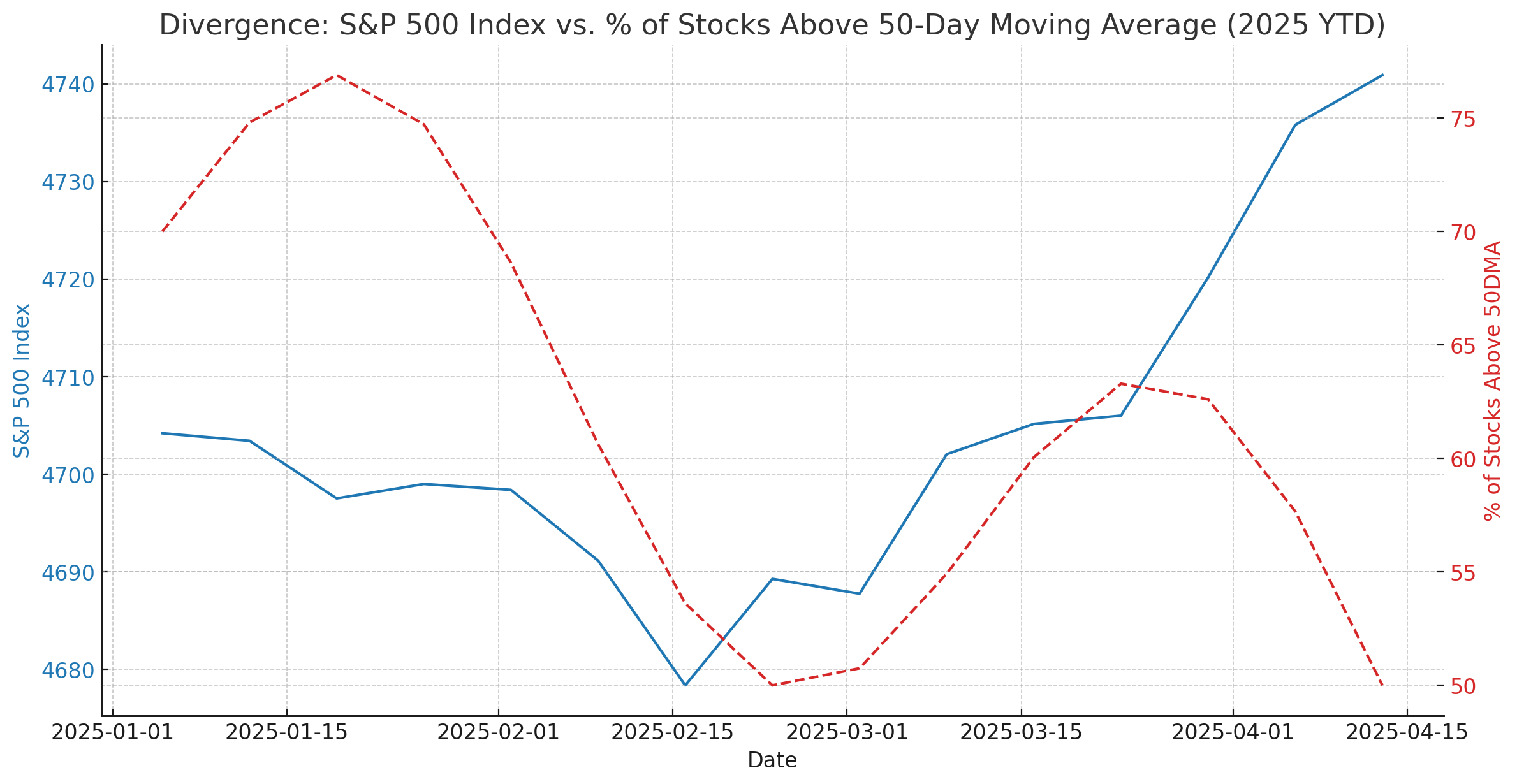

Equity Index Divergences

S&P 500: Up 6.5% YTD, driven by a narrow subset of mega-cap tech stocks.

Equal-Weighted S&P 500: Only +1.2% YTD, with over 52% of constituents trading below their 100-day MA.

Russell 2000: Flat YTD, underperforming due to rising refinancing risk and weaker earnings sentiment.

Institutional Implication: Passive flows remain concentrated in AI-levered equities. Active managers are quietly reducing exposure to small-cap cyclicals and shifting toward defensive quality and unleveraged balance sheets.

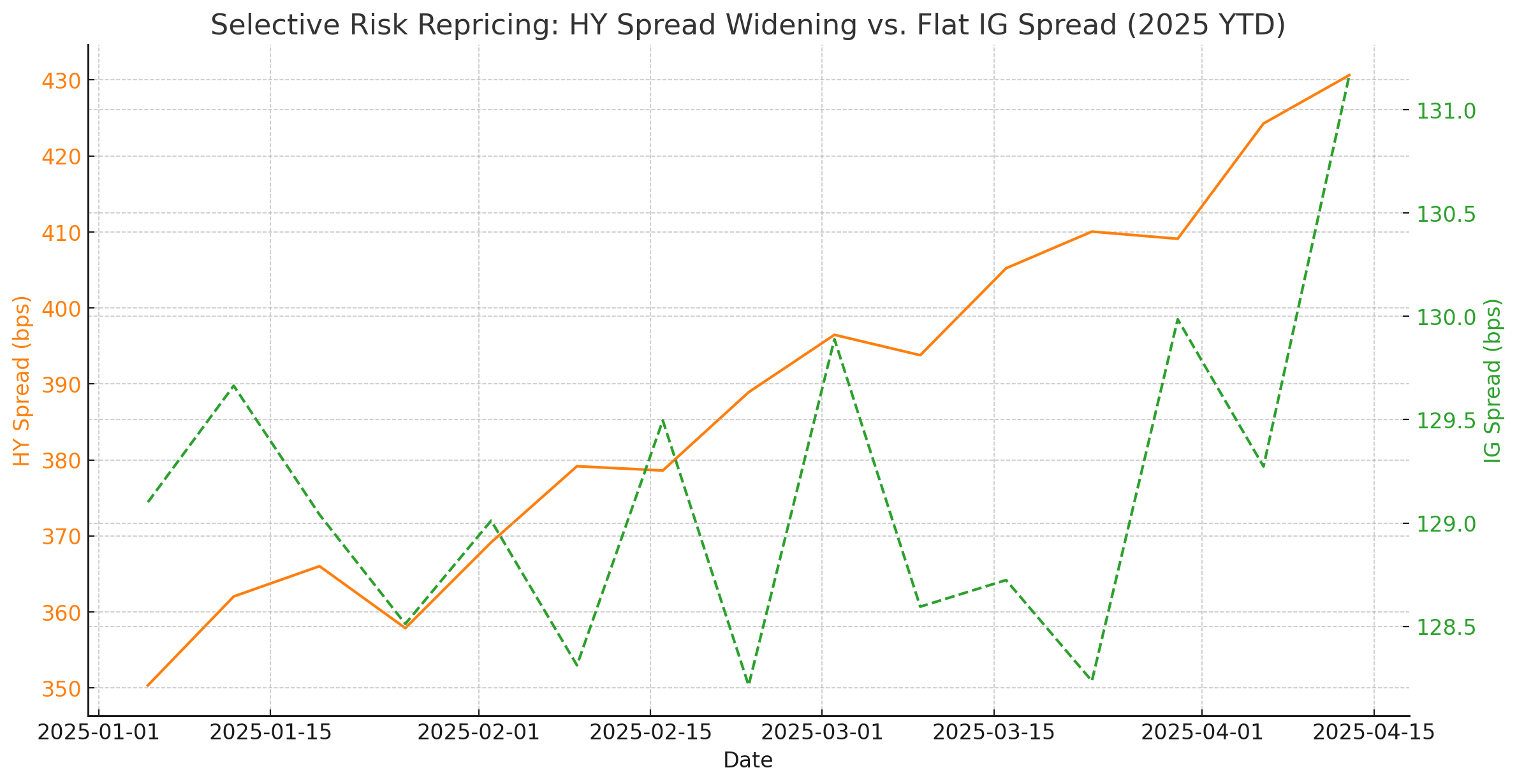

Credit Markets & Liquidity Outlook

High Yield OAS: Widened to 430bps, a +45bps move in two weeks, reflecting renewed credit stress pricing.

Investment Grade Spreads: Remain stable, but with rising issuance—corporates are front-running potential credit tightening.

Fed Liquidity Measures: Reverse Repo balances down to $300B, signaling passive liquidity bleed.

Watchpoint: The corporate credit complex may become the next volatility vector if rates stay elevated and profit margins compress further.

Institutional Positioning Trends: Rotations & Risk Offsets

1. Hedge Fund Activity

Gross Exposure: At 62% (Goldman PB), down 8% from Q1 peak.

Net Long Exposure: Rotating out of cyclicals, increasing allocations to staples, utilities, and long volatility structures.

Notable Build-Up: Long skew in S&P puts (1-3 months), coinciding with recent VIX divergence from equity strength.

2. Mutual Fund Allocations

Decreasing exposure to emerging markets, particularly China and Brazil, citing FX risk and political instability.

Rotating into short-duration treasuries and global infrastructure ETFs to hedge macro risk with yield.

3. Sovereign Wealth & Pension Activity

Increased Allocations: Into private credit and uncorrelated real assets (timberland, infrastructure, energy transition).

Reduced Weightings: From U.S. public equities to DM ex-U.S. industrials, seeking valuation resets and currency hedges.

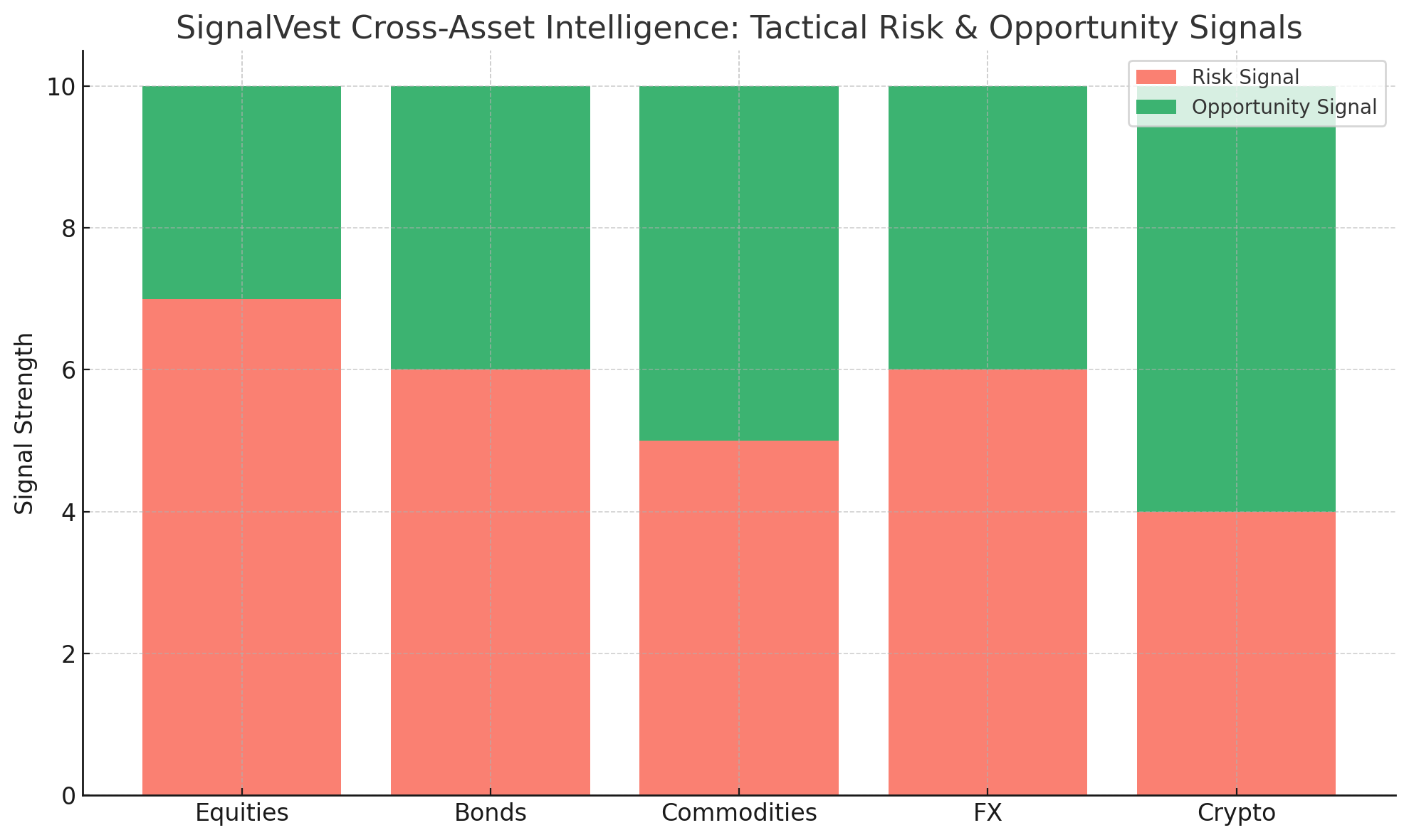

Cross-Asset Intelligence: Tactical Risk Observations

SignalVest Tactical Outlook: April–May 2025

🔻Risks to Watch:

Re-acceleration in inflation that sustains Fed hawkishness beyond June.

Soft earnings season outside mega-cap tech.

Liquidity shocks tied to regional bank refinancing or sovereign downgrades.

🔺Opportunities:

Relative value trades between growth vs. value and long-duration tech vs. short-duration industrials.

Long volatility, particularly in skewed or asymmetric ETF structures.

Event-driven trades around underfollowed earnings beats in mid-cap quality names.

Key Market Charts

Equity Breadth vs. S&P 500 Index (YTD 2025)

Credit Spread Movement (HY vs. IG)

Fed Rate Cut Expectations

SignalVest Positioning Radar

SignalVest models are currently overweight cash & equivalents (25%), neutral equities with a tilt toward U.S. quality large-cap, and long gold and short-duration bonds. We remain cautious on cyclicals, selective on international allocations, and are increasing screen time on asymmetric volatility structures ahead of Q2 earnings.

For institutional allocators, now is not the time for complacency based on index-level complacency. Liquidity fragility, uneven leadership, and quiet credit stress suggest preparing for event-driven volatility.

Stay Connected with SignalVest

To access our premium forensic equity risk reports, alerts on institutional positioning shifts, and exclusive trade ideas, upgrade to SignalVest Premium or reach out directly for custom advisory access.