SignalVest Insight | META’s AI Bet: Infrastructure, Incentives, and Illusions

Evaluating Capital Allocation, Insider Control, and Financial Integrity in Meta’s Post-Advertising Playbook

Revenue Recognition Practices

Meta recognizes revenue primarily from advertising contracts, billed when impressions or engagements occur, and from reality hardware and services as they are fulfilled. Key areas noted:

Advertising credits, incentives, and pricing fluctuations can introduce timing discretion

Reality Labs (Metaverse) sales are bundled with services and warranties, invoking multi-element arrangements and performance obligation judgments

Risk Note: While Meta complies with ASC 606, the layered judgment in revenue allocations and bundled recognition across AI, ads, and hardware opens potential for earnings smoothing — especially as Meta transitions between growth narratives.

Expense Capitalization & Long-Term Investment Visibility

Meta capitalizes significant infrastructure costs (data centers, AI accelerators, custom chips) tied to its long-term AI buildout.

Capital expenditures reached $32 billion in 2024 — the highest in company history.

These costs are depreciated across long lives, but revenue contribution from AI investments is still nascent.

Red Flag: There is a clear risk of under-realized ROI on CAPEX. Large capitalized bets into speculative segments (e.g., Reality Labs, open-source AI) can overstate current operating margins by deferring real risk into future periods.

Insider Control and Concentration

Mark Zuckerberg retains approx. 54% of voting control via dual-class shares.

Insider sales were lower in 2024 than prior years, but stock-based comp remains aggressive across R&D and G&A.

Board diversity and independence have improved, but governance remains asymmetric.

Interpretation: Control structures may suppress institutional pushback. Compensation alignment has improved post-2022 restructuring, but fundamental power asymmetry remains unaddressed.

Auditor's Report

Ernst & Young issued an unqualified opinion on both the financial statements and internal controls.

No Critical Audit Matters (CAMs) directly flagged, but disclosures note high estimation risk in:

Revenue recognition allocations

Deferred tax asset realization

Stock-based compensation

Watchpoint: Meta’s scale and disclosure quality pass clean audits — but investor over-reliance on reported segments without internal margin data (e.g., AI, Metaverse) increases narrative risk.

No Explicit Red Flags for Related Party Transactions or Off-Balance Items

No material disclosures of related-party transactions.

No visible off-balance sheet liabilities, variable interest entities (VIEs), or special-purpose vehicles.

Meta’s structural transparency remains industry-grade.

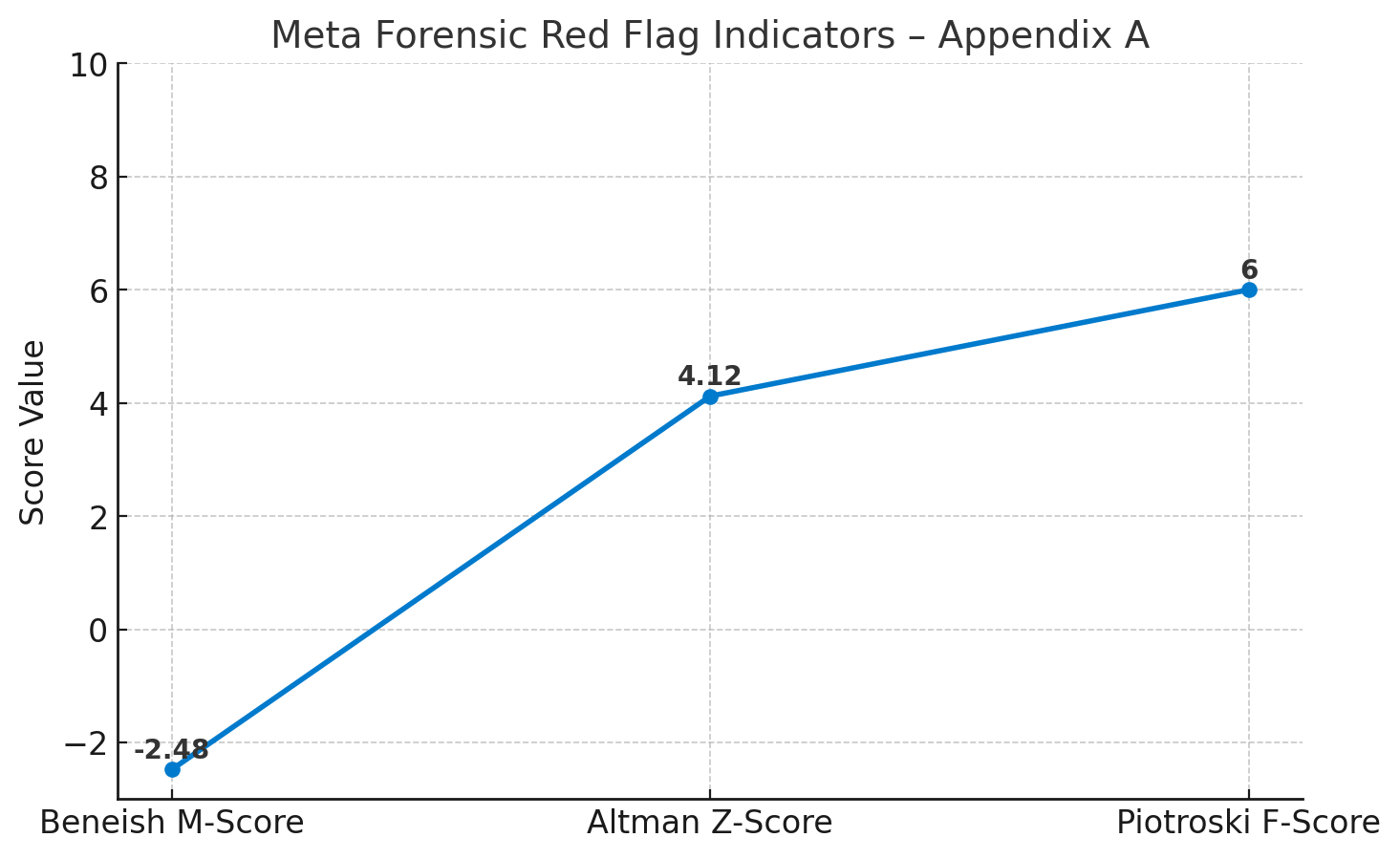

Appendix A — Forensic Red Flag Indicators