SignalVest Risk Watch | Freshpet (FRPT): Scaling Ambitions Meet Operational Strain

Freshpet (FRPT): Expansion Risks and Margin Pressures Emerge

While Freshpet (FRPT) continues to position itself as a high-growth leader in the premium pet food market, SignalVest forensic analysis uncovers rising operational and financial risks beneath the surface. Aggressive manufacturing expansion, persistent negative free cash flow, and insider selling patterns signal potential stress points that could undermine the growth narrative. In this SignalVest Risk Watch, we dissect the vulnerabilities emerging in Freshpet’s business model, highlight key risk pillars based on our proprietary Red Flag Intelligence framework, and assess the durability of its valuation premium under shifting macro and consumer conditions.

Freshpet, Inc. (FRPT) — a U.S.-based premium pet food company with a market capitalization of approximately $3.7 billion as of April 2025.

Date: April 28, 2025

Sector: Consumer Staples – Packaged Foods

Market Cap: ~$3.7 Billion

Exchange: NASDAQ

Executive Snapshot

Freshpet operates within the premium pet food segment, capitalizing on health-conscious trends for pets. While the growth narrative remains attractive, several risk vectors are emerging below the surface. SignalVest Risk Watch highlights vulnerabilities that could impact Freshpet’s valuation and operational resilience.

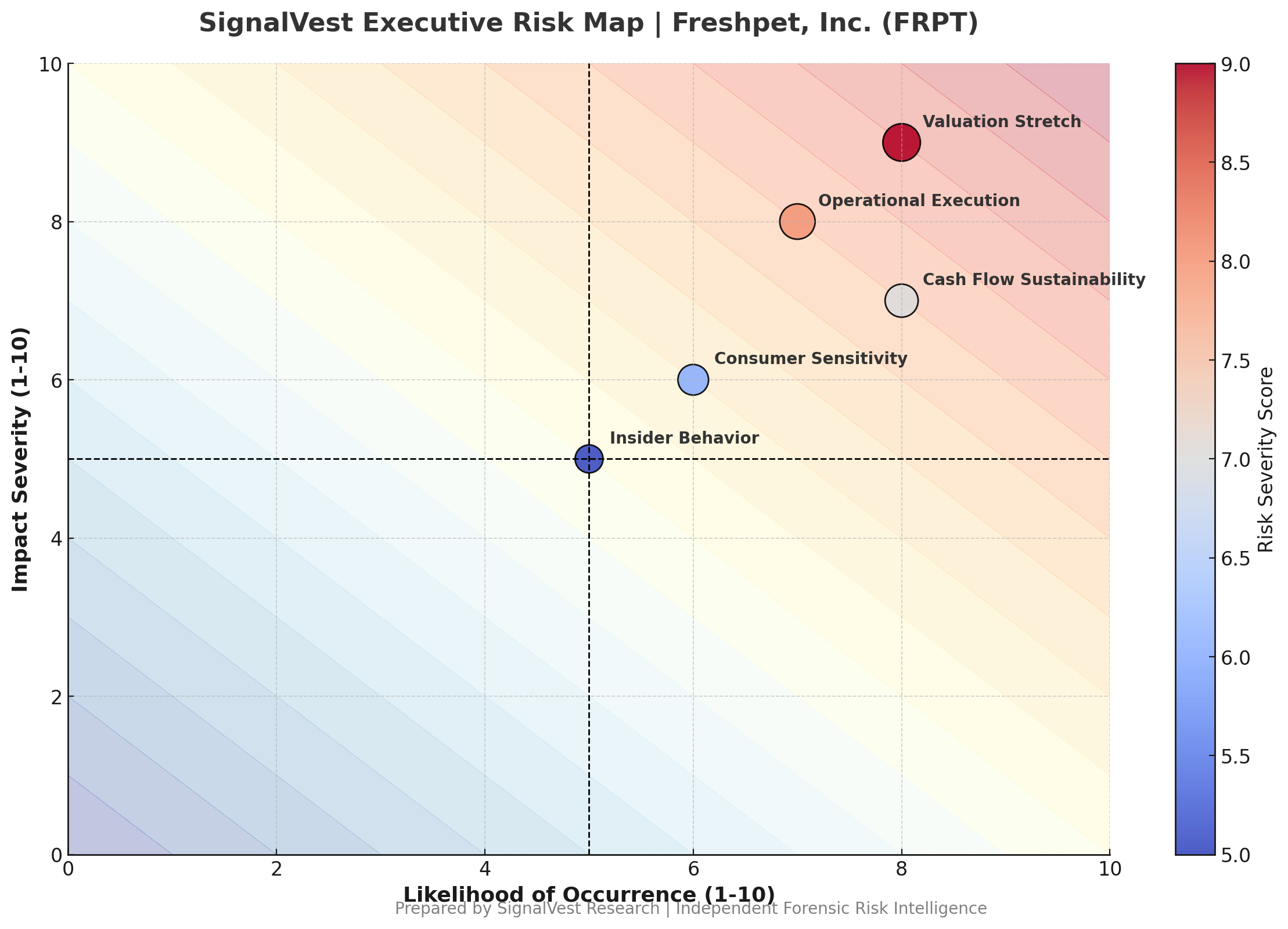

Top Risk Categories

Risk Area Assessment SignalVest Commentary Margin Compression - Moderate-High Raw material (meat) and logistics inflation still weigh on margins despite price increases. CapEx and Cash Burn - Moderate Freshpet’s aggressive expansion into new manufacturing facilities is capital intensive, putting pressure on free cash flow. Execution Risk - Moderate Complex scaling of refrigerated logistics and manufacturing facilities increases operational risks. Consumer Sensitivity - Moderate Premium pricing may face pushback if economic conditions deteriorate and pet owners trade down. Insider Selling Patterns - Emerging Increased insider sales over the past two quarters merit closer monitoring for alignment issues. Balance Sheet Leverage - Low Debt levels remain manageable post-recapitalization; however, monitoring is warranted if expansion continues. Valuation Stretch - High Trading at ~7.5x forward sales — valuation multiples assume uninterrupted hypergrowth, leaving little margin for error.

Key Financial Indicators (FY2024)

Metric Value Revenue $1.27 billion | Gross Margin 43.8% | EBITDA Margin 7.2% | Free Cash Flow -$42.5 million | Net Debt ~$160 million | Shares Outstanding YoY Growth +6% | Insider Transactions Net Sellers

Forensic Red Flag Highlights

CapEx Overruns: Freshpet’s Ennis, TX facility was delayed by six months, inflating build-out costs by 12% over initial estimates.

Negative Free Cash Flow: Even after top-line growth, cash generation remains negative, signaling dependency on external funding.

Product Recall Risk: Although no major recalls to date, Freshpet’s specialized refrigerated logistics introduce elevated risks compared to dry pet food peers.

Management Incentive Concerns: A shift toward growth-at-all-costs KPIs over profitability KPIs observed in the latest proxy filings.

Valuation Sensitivity: Current stock price implies sustained >20% annual revenue growth through 2028 — a high hurdle with no economic slack.

SignalVest Forensic Intelligence Scorecard

Model Result Interpretation Beneish M-Score -2.34 Below manipulation threshold (-2.22), but close enough to warrant continued surveillance. Altman Z-Score 5.28 Solid financial health, minimal bankruptcy risk currently. Piotroski F-Score 6/9 Moderate fundamental strength, but slipping cash metrics are an emerging concern.

SignalVest Watchlist Risk Classification:

Moderate Risk with Downside Sensitivity to Execution and Consumer Discretionary Trends

Visual Summary

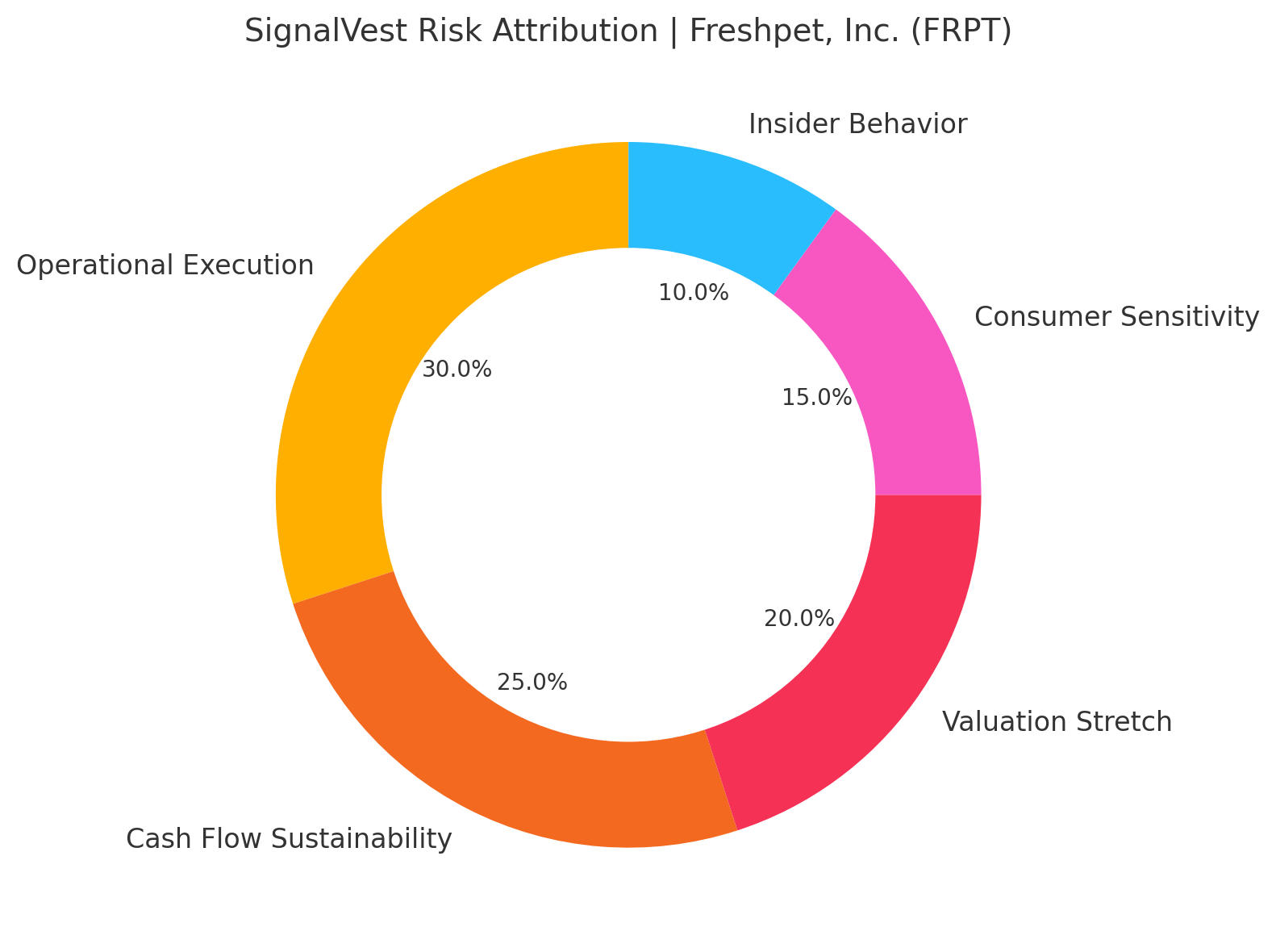

Donut Chart: Risk Attribution Breakdown

Risk Factor Weight (%) - Operational Execution 30% | Cash Flow Sustainability 25% | Valuation Stretch 20% | Consumer Sensitivity 15% | Insider Behavior 10%

Actionable Takeaways for Investors

Monitor CapEx Efficiency: Construction and expansion updates must be scrutinized quarterly to detect overruns early.

Watch Insider Selling Patterns: If insider sales persist while free cash flow remains negative, it could signal deteriorating internal confidence.

Stress-Test Revenue Sensitivity: Model revenue scenarios under moderate consumer spending pullbacks to assess valuation fragility.

Evaluate Scalability Risks: Freshpet’s dependency on specialized refrigerated infrastructure is a double-edged sword — it is a competitive moat but operationally brittle.

Reassess Growth Assumptions: If revenue growth decelerates below 15% YoY without material profitability improvements, downside revaluation risk grows meaningfully.

Prepared by:

SignalVest Research Division

Independent Forensic Financial Analysis | April 2025